Common Bookkeeping Mistakes And How To Avoid Them

Business bookkeeping duties can be the source of a lot of hassle for business owners. The piles of paperwork and stress over possible errors can add to big-time pressure, all created by common bookkeeping mistakes. How can you reduce tension and improve productivity at your workplace where bookkeeping is involved? What are the most common accounting errors? Equally important: How can accounting mistakes be corrected?

There’s no reason your business’s bookkeeping records have to bring you stress. Some mistakes may have minimal impact on a company’s financials and can be corrected. At the same time, other errors are more severe and could have a significant effect by misleading a company’s proper financial health. In the following, we’ll evaluate five of the most common accounting errors and how to avoid them.

1. Not discussing the bookkeeping terms with the accountant

People do not discuss the bookkeeping and accounting terms with the accountant before setting up for the first time. Often inexperience leads to extra time spent putting things right that you could have avoided with some training or assistance we can provide. Competent bookkeepers have the required expertise to find subtle mistakes that you might otherwise miss. As professionals, we will also be informed of the tax changes impacting your day-to-day financial practices. In the long run, getting a second set of eyes on your finances is highly beneficial and will save you time and money.

2. Not seeking help when needed

One of the most important things to know as a business owner is that you cannot do everything yourself. Maybe you are equipped to handle your bookkeeping and financial responsibilities. But, as a proprietor, you can always use some help in some fields such as accounting and bookkeeping responsibilities. Handing over the financial job to someone will give you more time and strength to explore the more significant development of your business. So if you are the new owner, appoint a professional, so you concentrate on the most important things. An external accountant can also advise identifying where to reduce expenses and help to prevent potential problems.

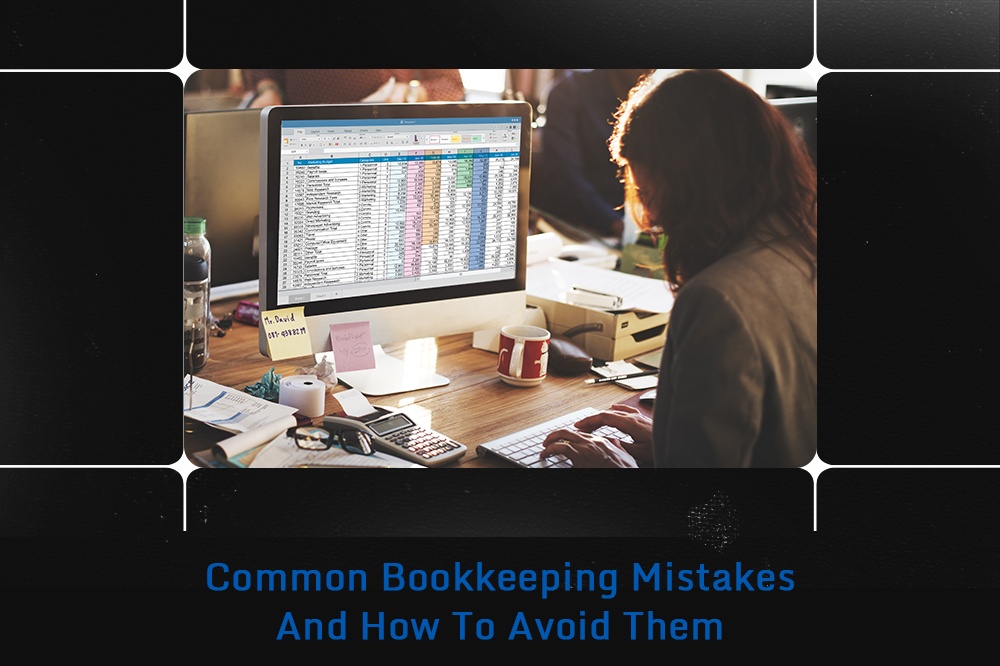

3. Not using one of the many accounting packages

Although excel takes care of some quick math, it’s still a person entering the numbers in, which sometimes involves errors humans may make. It puts a lot of pressure on those managing the spreadsheets and can be very costly for its success if mistakes occur. In short, A spreadsheet will likely only take you so far, which is when accounting software can assist you in making the step up. Accounting software is easy to use. Most of the hefty lifting has already been taken care of. This implies you will save time, as it doesn’t take long to get the team trained up. And you also save money, as you don’t require hiring an expert to understand the information.

4. Filing taxes late

It’s only sensible to file your taxes and payment on time, as the penalties are severe. If you forget to pay your taxes, the Canada Revenue Agency (CRA) can penalize you with a maximum of 25% of the total tax bill. You can ask for a filing extension to give you a little more time and dodge the fines in the worst-case scenario. But to even get a chance to file a tax-filing extension, you must pay some tax by the original due date. Our most important advice is to get your CPA to prepare and explain your sales tax responsibilities before starting a business. A qualified professional can help you understand your sales tax obligations, Know your sales tax filing deadlines and File your sales tax on or before the deadline.

5. Paying dividends instead of salary

The method you use to pay yourself from your business impacts many things – and not just your personal income tax owing. The form of your compensation can influence what you receive from government programs and your ability to pass for loans from lending institutions. Paying dividends removes the need to add to CPP, which reduces corporate and personal costs. The downside is that it does not allow you to contribute to the Canada Pension Plan. More cash now, less cash later. So choose wisely and don’t decide without first discussing with an accountant or lawyer. Consult with both before to ensure it is the right option, and if so, it takes the correct form and sets up the proper class of shares to allow for the future.

To hire the right booking-keeping company for your needs, reach out to Michael H. Keltz, Chartered Professional Accountant. Our professional staff's dedication to providing our clients with outstanding accounting and tax solutions makes our firm extraordinary. We customize our services according to the clients' needs, growth, and sector of activity. We also provide detailed record-keeping and give you the essential information you need to run your company and stimulate your profits.

We are serving clients across Leaside, East York, Toronto, Mississauga, Vaughan, Brampton, Markham, Oakville, Milton, Ajax, and the surrounding areas. To learn more about the services that we provide, please click here. If you’ve any questions about accounting and bookkeeping services, get in touch with us by clicking here.